Independent auditor's report

To: the Annual General Meeting of Shareholders and the Supervisory Board of Koninklijke DSM N.V.

Report on the audit of the financial statements 2018 included in the Integrated Annual Report

Our opinion

In our opinion:

- the accompanying consolidated financial statements give a true and fair view of the financial position of Koninklijke DSM N.V. (hereafter: Royal DSM) as at 31 December 2018 and of its result and its cash flows for the year then ended, in accordance with International Financial Reporting Standards as adopted by the European Union (EU-IFRS) and with Part 9 of Book 2 of the Dutch Civil Code.

- the accompanying parent company financial statements give a true and fair view of the financial position of Royal DSM as at 31 December 2018 and of its result for the year then ended in accordance with Part 9 of Book 2 of the Dutch Civil Code.

What we have audited

We have audited the financial statements 2018 of Royal DSM based in Heerlen. The financial statements include the consolidated financial statements and the parent company financial statements.

The consolidated financial statements comprise:

- the consolidated balance sheet as at 31 December 2018;

- the following consolidated statements for 2018: the income statement, the statements of comprehensive income, changes in equity and cash flows; and

- the notes comprising a summary of the significant accounting policies and other explanatory information.

The parent company financial statements comprise:

- the parent company balance sheet as at 31 December 2018;

- the parent company income statement for 2018; and

- the notes comprising a summary of the accounting policies and other explanatory information.

Basis for our opinion

We conducted our audit in accordance with Dutch law, including the Dutch Standards on Auditing. Our responsibilities under those standards are further described in the 'Our responsibilities for the audit of the financial statements' section of our report.

We are independent of Royal DSM in accordance with the EU Regulation on specific requirements regarding statutory audits of public-interest entities, the 'Wet toezicht accountantsorganisaties' (Wta, Audit firms supervision act), the 'Verordening inzake de onafhankelijkheid van accountants bij assurance-opdrachten' (ViO, Code of Ethics for Professional Accountants, a regulation with respect to independence) and other relevant independence regulations in the Netherlands. Furthermore, we have complied with the 'Verordening gedrags- en beroepsregels accountants' (VGBA, Dutch Code of Ethics).

We believe the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Audit approach

Summary

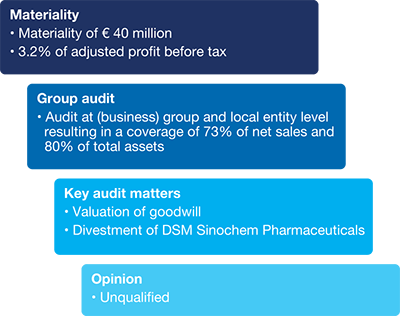

Materiality

Based on our professional judgement we determined the materiality for the financial statements as a whole at €40 million (2017: €30 million). The materiality is determined with reference to adjusted profit before tax (Note 2: €1,244 million; 2017: €853 million) of which it represents 3.2% (2017: 3.5%). In addition, the appropriateness of the materiality was assessed by comparing the amount to consolidated net sales of which it represents 0.4% (2017: 0.3%). We have also taken into account misstatements and/or possible misstatements that in our opinion are material for qualitative reasons for the users of the financial statements.

We agreed with the Supervisory Board that misstatements in excess of €1.5 million (2017: €1 million) which are identified during the audit, would be reported to them, as well as smaller misstatements that in our view must be reported on qualitative grounds.

Scope of the group audit

Royal DSM is at the head of a group of reporting entities (hereafter: entities). The financial information of this group is included in the financial statements of Royal DSM.

Because we are ultimately responsible for the auditor's report, we are also responsible for directing, supervising and performing the group audit. In this respect we have determined the nature and extent of the audit procedures to be carried out for entities reporting for group audit purposes. Decisive were the size and/or the risk profile of the entities or operations. On this basis, we selected 22 entities (2017: 25 entities) to perform audits for group reporting purposes on a complete set of financial information as well as 17 entities (2017: 17 entities) to perform specified audit procedures for group reporting purposes on specific items of financial information.

This resulted in a coverage of 73% (2017: 73%) of total net sales and 80% (2017: 80%) of total assets. The remaining 27% of total net sales (2017: 27%) and 20% of total assets (2017: 20%) is represented by a significant number of entities ('Remaining entities'), none of which individually represents more than 2% of total net sales and 1% of total assets.

For these remaining entities, we performed amongst others analytical procedures at (business) group level to validate our assessment that there are no significant risks of material misstatement within these entities.

The audit coverage as stated above can be further specified as follows:

We have:

- performed audit procedures ourselves at (business) group level in respect of areas such as the annual goodwill impairment tests, other (in)tangible asset impairments, accounting for associates and joint ventures, valuation of deferred tax assets, acquisitions, disposals, restructurings, treasury and shared service centers; and

- used the work of local KPMG auditors when auditing or performing specified audit procedures at business group and local entity level;

The group audit team has set materiality levels for the entities, which ranged from €5 million to €12.5 million (2017: €5 million to €12.5 million), based on the mix of size and risk profile of the entities within the group.

The group audit team provided detailed instructions to all business group and local entity auditors part of the group audit, covering the significant audit areas, including the relevant risks of material misstatement, and the information required to be reported back to the group audit team. The group audit team visited entity locations in the United States of America, Switzerland, China, Brazil and the shared service center in India.

Telephone conferences were held with all entity auditors part of the group audit. During these visits and telephone conferences, we discussed the audit approach and the audit findings and observations reported to the group audit team. For a number of these entities we also performed file reviews.

By performing the procedures mentioned above at reporting entities, together with additional procedures at (business) group level, we have been able to obtain sufficient and appropriate audit evidence about the group's financial information to provide an opinion about the financial statements.

Audit scope in relation to fraud

In accordance with the Dutch Standards on Auditing we are responsible for obtaining reasonable assurance that the financial statements taken as a whole are free from material misstatement, whether caused by fraud or error. As part of our fraud risk assessment we:

- made use of management's evaluation in relation to fraud risk management (prevention, detections and response);

- assessed Royal DSM's entity level controls which include ethical standards to create a culture of honesty;

- assessed events or conditions that indicate an incentive or pressure to commit fraud or provide an opportunity to commit fraud ('fraud risk factors'); and

- involved a KPMG forensic specialist.

Based on our fraud risk assessment, we have not identified any fraud risks in addition to those presumed by the Auditing Standards. Those presumed risks were relevant to our audit and have been discussed with the Managing and Supervisory Board, and are as follows:

- fraud risk in relation to revenue recognition, specifically being the risk of manual override with respect to the cut-off of revenue for the period prior to the financial year-end; and

- fraud risk in relation to management override of controls to meet targets and/or expectations.

Our audit procedures included an evaluation of the design and implementation of internal controls relevant to mitigate these fraud risks and supplementary substantive audit procedures, including detailed testing of high risk journal entries, inspection and testing of documentation such as agreements with the customer and shipping documents, in relation to the correct recognition of revenues for the period prior to the financial year-end and an evaluation of key estimates and judgment by management.

Our audit procedures differ from a specific forensic fraud investigation, which investigation often has a more in-depth character.

Our key audit matters

Key audit matters are those matters that, in our professional judgement, were of most significance in our audit of the financial statements. We have communicated the key audit matters to the Supervisory Board. The key audit matters are not a comprehensive reflection of all matters discussed.

These matters were addressed in the context of our audit of the financial statements as a whole and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

Compared to last year we have added as a key audit matter the divestment of Royal DSM's investment in DSM Sinochem Pharmaceuticals as the accounting for this transaction is significant for the financial statements. Last year's key audit matters about the Impairment of joint venture POET – DSM Advanced Biofuels LLC and the Divestment of Patheon N.V. are not included anymore in 2018, given the decreased risk profile of the valuation of DSM's investment in POET – DSM Advanced Biofuels LLC and the one-off nature of the divestment of Patheon N.V.

Valuation of goodwill

Description

Royal DSM carries a significant amount of goodwill in the balance sheet. Under EU-IFRSs, Royal DSM is required to test the amount of goodwill for impairment at least annually. The impairment tests were significant to our audit due to the complexity of the assessment process and judgments and assumptions involved which are affected by expected future market and economic developments.

Our response

We challenged the cash flow projections included in the annual goodwill impairment tests. Our audit procedures included, amongst others, the involvement of a valuation specialist to assist us in evaluating the assumptions, in particular the terminal growth and pre-tax discount rates, and the valuation methodology used by Royal DSM. We furthermore assessed the appropriateness of other data used by comparing them to external and historical data, such as external market growth expectations and by analyzing sensitivities in Royal DSM's valuation model. We specifically focused on the sensitivity in the available headroom for the cash generating units, evaluating whether a reasonably possible change in key assumptions could cause the carrying amount to exceed its recoverable amount and assessed the historical accuracy of management's estimates. We assessed the adequacy of the disclosure (Note 8) to the financial statements.

Our observation

We consider management's key assumptions and estimates to be within the acceptable range and we assessed the disclosure (Note 8) to the financial statements as being proportionate.

Divestment of DSM Sinochem Pharmaceuticals

Description

On 31 October 2018 Royal DSM completed the sale of its investment in DSM Sinochem Pharmaceuticals. This sale resulted in a gain on disposal of €109 million. Given the amounts involved as disclosed in Note 10 to the financial statements, the accounting for this transaction is significant for the financial statements.

Our response

We tested the accuracy and completeness of the gain on the disposal by comparing the consideration received with the terms and conditions according to the Share Purchase Agreement (SPA), the cash receipts and by reconciling the book value of the disposed amount to the underlying accounting records. We verified whether the gain on disposal was calculated in accordance with the relevant clauses of the SPA underlying the transaction. When verifying the gain on disposal we assessed the net present value of the earn-out receivable which is linked to future performance of the divested business. We also evaluated the adequacy of the disclosure (Note 10) of this disposal in the financial statements.

Our observation

We consider that the gain on disposal is appropriately reflected in the financial statements and we assessed the disclosure (Note 10) to the financial statements as being proportionate.

Report on the other information included in the Integrated Annual Report

In addition to the financial statements and our auditor's report thereon, the Integrated Annual Report contains other information that consists of:

- Report by the Managing Board which includes the chapters Key data, Letter from the CEO, Report by the Managing Board, Review of business, Reporting policies and Corporate governance and risk management;

- Report by the Supervisory Board which includes the chapters Report by the Supervisory Board and Supervisory Board and Managing Board Royal DSM;

- Other information pursuant to Part 9 of Book 2 of the Dutch Civil Code;

- Other information which consists of the chapters What still went wrong in 2018, Information about the DSM share, Sustainability statements, DSM figures: five-year summary and Explanation of some concepts and ratios.

Based on the following procedures performed, we conclude that the other information:

- is consistent with the financial statements and does not contain material misstatements; and

- contains the information as required by Part 9 of Book 2 of the Dutch Civil Code.

We have read the other information. Based on our knowledge and understanding obtained through our audit of the financial statements or otherwise, we have considered whether the other information contains material misstatements.

By performing these procedures, we comply with the requirements of Part 9 of Book 2 of the Dutch Civil Code and the Dutch Standard 720. The scope of the procedures performed is substantially less than the scope of those performed in our audit of the financial statements.

The Managing Board is responsible for the preparation of the other information, including the Report by the Managing Board in accordance with Part 9 of Book 2 of the Dutch Civil Code and the other information pursuant to Part 9 of Book 2 of the Dutch Civil Code.

Report on other legal and regulatory requirements

Engagement

We were engaged by the Annual General Meeting of Shareholders as auditor of Royal DSM on 7 May 2014, as of the audit for the year 2015 and have operated as statutory auditor ever since that financial year.

No prohibited non-audit services

We have not provided prohibited non-audit services as referred to in Article 5(1) of the EU Regulation on specific requirements regarding statutory audits of public-interest entities.

Description of responsibilities regarding the financial statements

Responsibilities of the Managing Board and the Supervisory Board for the financial statements

The Managing Board is responsible for the preparation and fair presentation of the financial statements in accordance with EU-IFRS and Part 9 of Book 2 of the Dutch Civil Code. Furthermore, the Managing Board is responsible for such internal control as the Managing Board determines is necessary to enable the preparation of the financial statements that are free from material misstatement, whether due to fraud or error.

As part of the preparation of the financial statements, the Managing Board is responsible for assessing Royal DSM's ability to continue as a going concern. Based on the financial reporting frameworks mentioned, the Managing Board should prepare the financial statements using the going concern basis of accounting unless the Managing Board either intends to liquidate the company or to cease operations, or has no realistic alternative but to do so. The Managing Board should disclose events and circumstances that may cast significant doubt on the company's ability to continue as a going concern in the financial statements.

The Supervisory Board is responsible for overseeing Royal DSM's financial reporting process.

Our responsibilities for the audit of the financial statements

Our objective is to plan and perform the audit engagement in a manner that allows us to obtain sufficient and appropriate audit evidence for our opinion.

Our audit has been performed with a high, but not absolute, level of assurance, which means we may not detect all material errors and fraud during our audit.

Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements. The materiality affects the nature, timing and extent of our audit procedures and the evaluation of the effect of identified misstatements on our opinion.

A further description of our responsibilities for the audit of the financial statements is included in appendix to this auditor's report. This description forms part of our auditor's report.

Amstelveen, 7 March 2019

KPMG Accountants N.V.

E.H.W. Weusten RA

Appendix: Description of our responsibilities for the audit of the financial statements

We have exercised professional judgement and have maintained professional skepticism throughout the audit, in accordance with Dutch Standards on Auditing, ethical requirements and independence requirements. Our audit included among others:

- identifying and assessing the risks of material misstatement of the financial statements, whether due to fraud or error, designing and performing audit procedures responsive to those risks, and obtaining audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than the risk resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control;

- obtaining an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of Royal DSM's internal control;

- evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by the Managing Board;

- concluding on the appropriateness of the Managing Board's use of the going concern basis of accounting, and based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on Royal DSM's ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor's report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor's report. However, future events or conditions may cause a company to cease to continue as a going concern;

- evaluating the overall presentation, structure and content of the financial statements, including the disclosures; and

- evaluating whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with the Supervisory Board regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant findings in internal control that we identify during our audit. In this respect we also submit an additional report to the audit committee in accordance with Article 11 of the EU Regulation on specific requirements regarding statutory audits of public-interest entities. The information included in this additional report is consistent with our audit opinion in this auditor's report.

We provide the Supervisory Board with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with the Supervisory Board, we determine the key audit matters: those matters that were of most significance in the audit of the financial statements. We describe these matters in our auditor's report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, not communicating the matter is in the public interest.